You can pay your bills in a multitude of ways these days. Venmo, Zelle, ACH transfers, credit cards, debit cards, mobile wallets, and instant peer-to-peer apps have made digital payments the default for most everyday transactions. Checks are widely thought of as a thing of the past. But are they really? The data tells a more nuanced story. While check usage has declined sharply over the past two decades, checks still play a meaningful role in specific situations, and millions of Americans continue to write them every month for rent, taxes, contractor payments, charitable donations, and gifts. This guide answers the question directly, with current data from the Federal Reserve, Pew Research, and the American Bankers Association. It also covers when checks still make sense, how to write one safely, and what the future of paper checks looks like as digital payment options continue to expand. So, people still write checks?

Checks may only be 7% of all non-cash payments, and if you’re under 30, you’ll probably never write a check; but technology makes checks more fraud-proof, and the more you know about checks, and when you can use them, the better equipped you will be to take advantage of what they still offer. They will be better. In addition, new developments such as check printing software have made the check-writing process easier to understand, and now it is easier than ever to take advantage of what checks can still offer.

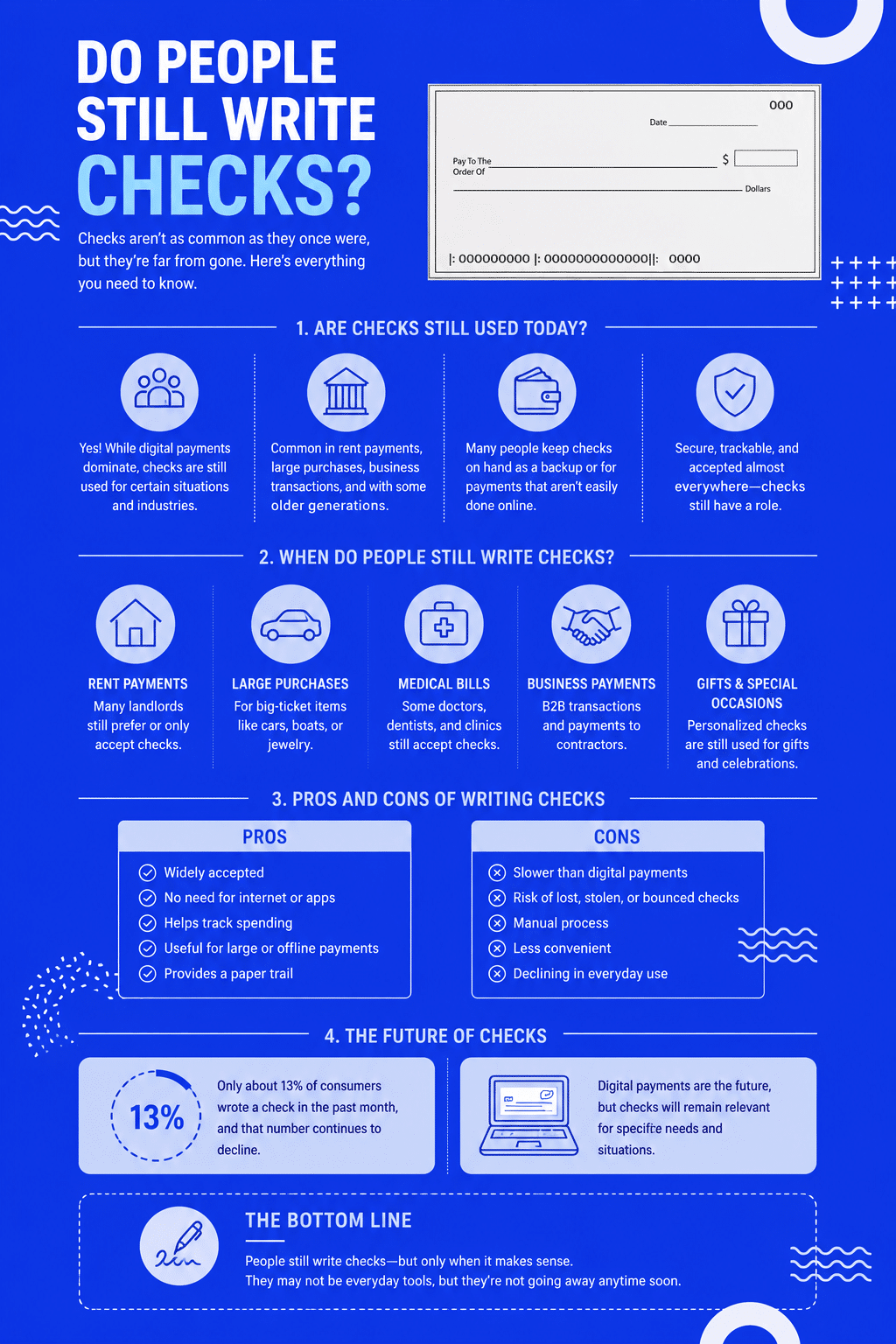

Do People Still Write Checks? The Current Data

The short answer is yes, but far fewer than in past decades, and the decline continues steadily year over year.

According to the Federal Reserve Payments Study, the most comprehensive recurring research on US payment habits, check usage has been declining at roughly 7 to 8 percent per year for much of the past decade. By the time of the most recent study, checks accounted for a small single-digit percentage of total non-cash payments by number of transactions, a dramatic decline from their once-dominant position. The number of checks written in the US fell from approximately 41.9 billion in 2000 to under 12 billion in recent measurement periods.

That decline tells one part of the story. The other part is who is still writing checks, and why. Research from the Federal Reserve Bank of San Francisco’s Diary of Consumer Payment Choice consistently shows that:

- Older Americans write more checks than younger Americans. Adults aged 55 and over write checks at significantly higher rates than younger generations, and account for a large share of all checks written today.

- Higher-dollar transactions are more likely to be paid by check. Checks remain disproportionately used for transactions over $200, including rent, mortgage payments, contractor invoices, taxes, and charitable contributions.

- Specific industries still rely on checks. Property management, small contractor services, some local government transactions, charitable organizations, and small businesses that want to avoid card processing fees continue to receive and process checks at meaningful volumes.

- Geographic and digital access differences matter. According to the Pew Research Center’s most recent data on internet use, a small percentage of US adults still do not use the internet, with rates higher among older adults, those with lower household incomes, and those in some rural areas. For these households, checks may remain the most practical bill-payment method available.

So while the trend is clearly toward digital payments, checks have not disappeared. They have shifted from being a default everyday payment tool to a specific-use instrument that serves particular transactions, demographics, and contexts where digital alternatives are unavailable, inconvenient, or more expensive.

What Are Checks and Where Do You Get Them?

Personal checks work very much like debit cards, except you have to wait for them to work for a much longer period.

Instead of the money immediately being taken from your account, the money you pay on a check comes out only after cashing the check. If someone takes a few days or weeks to cash the check; the money will stay in your account until they decide to go forward with the deposit.

You can order checks from your bank, and some banks will give you a free checkbook. Others will make you pay for every check you order. You can also get checks online by using check printing software.

When Will You Use a Personal Check?

People still write checks, and checks are not an outdated payment method, but they certainly have lost some utility. That doesn’t mean they don’t have their place in the world. In some ways, personal checks can be the only way to pay a bill. Some smaller businesses still accept checks, and many landlords and real estate owners prefer checks. You can pay your taxes by check, and some companies may charge you extra for paying your bill with a credit card. So, there is no fee for using a check.

For those offline, checks can be a helpful way to keep track of their finances. In fact, according to a 2021 report by the Pew Research Center, 7% of adult Americans don’t use the internet. In addition, 19% of households making less than $30,000 also don’t use the internet. So if you live in a home without internet access, paying your bills by check might be the only option.

When Checks Still Make Practical Sense in 2026

Beyond the general decline in check usage, there are specific situations where writing a check remains either the best or only practical option.

- Rent payments to small landlords. While large property management companies typically offer online payment portals, many small landlords still prefer checks, partly to avoid payment processing fees and partly because they create a clear paper trail with the date, amount, and memo line documenting what the payment was for.

- Federal and state tax payments. The IRS and most state tax authorities accept paper checks for tax payments. While electronic payment is generally faster and provides automatic confirmation, mailing a check remains a valid and widely-used option, particularly for quarterly estimated tax payments.

- Contractor and service provider payments. Small contractors, freelancers, and service providers (plumbers, electricians, lawn care professionals, house cleaners) often prefer checks because they avoid credit card processing fees, which can be 2 to 3 percent of the transaction value.

- Charitable contributions. Many charitable organizations, particularly local and smaller nonprofits, prefer or exclusively accept checks for donations. Writing a check also creates a tangible record for tax-deduction documentation purposes.

- Cash gifts and wedding gifts. Checks remain a common format for wedding gifts, graduation gifts, and other personal cash gifts because they feel more formal than handing over cash and do not require the recipient to share banking details for an electronic transfer.

- Closing on real estate transactions. While digital escrow and wire transfers have become the standard for the bulk of real estate payments, some smaller transactions and earnest money deposits still use cashier’s checks or personal checks.

- Situations where the recipient does not accept digital payment. Some smaller businesses, older organizations, court fees, certain HOA fees, and other recipients simply do not have digital payment infrastructure in place. In these cases, a check may be the only option offered.

- Avoiding credit card or processing fees. Some businesses charge a convenience fee for credit card or digital payments. A check often avoids this fee entirely.

Parts of a Check

The following section breaks down checks into their respective components. Your name and mailing address usually appear on the top left corner of each check and identify who sent the check. Next, find the check number in the upper right corner. First, your check number helps the bank and whoever else needs to use the check track. Finally, you have to pay at the order line in the middle of the check.

“The pay to the order of” line describes the party to who the check addresses. To the right of this line, you will write the payment amount for the check. Directly below the pay to the order line is another unlabeled line where you will write the check amount in words. For example, if you write $300 in the amount box, you will spell out three hundred dollars on the amount line.

The signature line is on the lower right of the check, and this is where you will sign the check. After signing the check, it becomes a legally negotiable instrument that the recipient can deposit or cash. To the left of this line is the memo line, where you will have the option of making a notation for anyone involved in the check process.

At the bottom of the check is a set of numbers that help you move your payment. The American Bankers Association bank routing number is the first set on the left. This nine-digit number identifies the financial institution that paid for your transaction and instructs the bank to release your funds in the correct amount to the recipient. The account number and the check number appear with the bank routing number, so you have a trail for your account.

Understanding the MICR Line and Check Number Sequencing

The set of numbers at the bottom of every check is printed in a special font called MICR (Magnetic Ink Character Recognition). The ink itself contains iron oxide, which can be read by bank scanning equipment even if the check is creased, marked, or partially obscured. This is why those numbers always look slightly different from the rest of the printing on a check.

The MICR line contains three pieces of information in a specific order: the bank routing number (nine digits identifying your financial institution), your account number, and the check number. Your check number sequence helps both you and your bank track which checks have been written, which have cleared, and which are still outstanding. Most personal checkbooks start at check number 1001 rather than 0001, which is a convention that signals the account holder has some banking history, particularly to merchants who may be more cautious about accepting very low-numbered checks from new accounts.

There Is More than One Way to Sign

Contrary to what you might believe, checks are still the preferred payment method for businesses to their employees. So, if your employer doesn’t offer direct deposit or you’re a freelance worker, you might get paid with a check. Checks can also be an effective way for individuals to pay each other when trying to give someone money as a gift.

When you get a check, you can sign the back of it to cash it or deposit it into your bank account. You will likely want to sign; or endorse the back of the check as your name appears on the pay-to-order line. If you want to deposit the check; you can add a layer of security by writing “deposit only” underneath your signature. This tells the bank not to give anyone cash for the check but to pay the funds into your listed account.

If you deposit the check using a mobile device, you will need to endorse the check fully, and you should name the financial institution. Doing so will prevent multiple deposits of the same check into different accounts.

Check Etiquette

Many stores accept checks for payment with proper identification. However, store clerks and owners will likely become annoyed if you spend too much time filling out your check; especially if there’s a long line behind you. So if you know, you’ll use a check for an in-store purchase, fill out the parts you can; and leave the amount and signature fields blank until you have your purchase total.

How Long Does a Check Stay Valid?

One of the most commonly searched questions about checks is how long they remain valid after being written, since this affects both check writers and check recipients.

Most US banks follow a standard practice of treating personal checks as “stale-dated” after six months from the date written on the check. A stale-dated check is one the bank is not obligated to honor, though in practice many banks will still process older checks at their discretion. If you receive a check that is more than six months old, the safer approach is to contact the issuer and request a fresh replacement check rather than attempting to deposit the original.

Different check types follow different rules:

- Personal checks: Generally treated as stale after six months.

- Business checks: Some businesses print “Void after 90 days” or similar language on their checks, which makes the check invalid after that date regardless of bank policy.

- Cashier’s checks: Generally do not expire in the same way personal checks do, though state laws on unclaimed property may apply if a cashier’s check goes uncashed for an extended period (often one to three years depending on the state).

- US Treasury checks (tax refunds, Social Security, etc.): Valid for one year from the date of issue.

- State and government checks: Validity varies by state, but most are valid for at least one year, with some states allowing longer.

If you discover an old check that you wrote and never had cashed, contact your bank to place a stop payment to ensure it cannot be cashed unexpectedly later. Stop payment orders typically last six months and can be renewed.

Frequently Asked Questions About Checks

Yes, personal and business checks remain a legally recognized payment method in the United States. The Uniform Commercial Code (UCC) Article 3, which governs negotiable instruments, provides the legal framework for checks and is in effect across all states. As long as a check is properly written, signed, and presented within the validity period, banks are required to process it under standard banking regulations. Checks remain particularly common for rent payments, tax payments, charitable donations, contractor payments, and personal gifts.

While exact percentages vary by survey and methodology, recent data from the Federal Reserve Payments Study and consumer payment diaries from the Federal Reserve Bank of San Francisco indicate that a meaningful minority of US adults still write checks at least occasionally, with usage concentrated among older adults and for higher-value transactions. Checks now represent a small single-digit percentage of total noncash payments by transaction count, a significant decline from their once-dominant position but still representing billions of transactions per year. Many Americans who rarely use checks for everyday purchases still write occasional checks for specific situations like rent, charitable giving, or gifts.

To write a check correctly, fill in six fields in sequence: the date (today’s date in the upper right), the payee (the full legal name of the person or business you are paying), the numeric dollar amount (in the small box on the right), the written dollar amount (spelled out on the long line, with cents as a fraction over 100), an optional memo (briefly describing what the payment is for), and your signature (in the lower right). For full step-by-step guidance on writing checks safely and avoiding common fraud risks, see our companion guide on things to know before writing your next check.

A personal check is drawn against the funds in your individual checking account. When the recipient deposits the check, the bank verifies that your account has sufficient funds before clearing it, which is why personal checks can bounce if you do not have enough money in your account. A cashier’s check is drawn against the bank’s own funds. To get one, you pay the bank the face value of the check upfront, and the bank guarantees the funds. Because cashier’s checks are pre-funded by the bank rather than the individual, they are considered more secure and are often required for high-value transactions like real estate closings, car purchases, or large deposits.

Yes, personal checks can bounce if the account they are drawn against does not have sufficient funds at the time the check is presented. When a check bounces, the recipient’s bank typically returns it marked NSF (non-sufficient funds), and both the check writer and the recipient may face fees from their respective banks. The check writer may also face additional consequences depending on state law, including potential criminal charges in some cases for writing checks with intent to defraud. To avoid bounced checks, keep accurate records of your account balance, account for any pending transactions before writing a check, and consider linking overdraft protection from a savings account if available.

Both methods have security tradeoffs. Digital payments offer protections like instant transaction confirmation, automatic record-keeping, fraud monitoring, and reversal options under regulations like Regulation E. Checks have a documented paper trail, do not require sharing bank login credentials, and create a physical record useful for tax documentation. However, checks are more vulnerable to specific fraud types including check washing (where fraudsters alter the payee or amount using chemical solvents) and mail theft. For most everyday transactions, digital payment is generally faster and at least as secure as a check. For specific transactions like rent payments to small landlords or contractor payments, a check may be the only option offered or may be preferred by the recipient.

Probably not in the foreseeable future, despite the steady decline in usage. Checks remain embedded in specific transaction types (rent, contractor payments, tax payments, charitable giving) and in the financial habits of certain demographics, particularly older adults. They also serve as a fallback for situations where digital payment is unavailable or inconvenient. While check usage will likely continue declining year over year as digital options expand, the complete elimination of checks would require coordinated changes across millions of small businesses, landlords, and financial institutions that currently rely on them as a primary or backup payment method.

Conclusion: People Still Write Checks, Just Less Often

The honest answer to the question is yes, people still write checks, but far fewer than two decades ago. What was once the default method for paying bills, rent, and routine purchases has shifted into a specific-use payment instrument that serves particular transactions and contexts where digital alternatives are unavailable, inconvenient, or more expensive.

Understanding when checks still make sense (rent to small landlords, contractor payments, charitable contributions, tax payments, personal gifts) and when digital payments are the better choice (most everyday purchases, peer-to-peer transfers between connected accounts, recurring bills) helps you use each method effectively rather than treating them as either-or.

If you do write checks occasionally, knowing how to write them correctly and safely matters more than ever, given the documented rise in check fraud since 2020. Our guide on things to know before writing your next check covers the specific precautions that protect both you and the recipient. For broader financial habits that support strong personal and business money management, key bookkeeping activities for strong financial management covers the recordkeeping practices that complement check writing and digital payments alike.

Paper checks will probably continue declining in volume year over year. But for the specific transactions where they still serve a purpose, understanding how they work, when to use them, and how to use them safely remains genuinely useful knowledge.

Infographic